A reader asks:

I recently started looking at my mother-in-law’s retirement account. She’s been with [advisor name redacted] since October 2010 and has a 2.61% annual return. According to their chart, the S&P 500 had a 12.95% annual return during that same period. While I know she shouldn’t expect a return equal to the S&P 500 since she’s not all equities (she’s in 60% stocks, 40% bonds), it’s frustrating how much she’s underperformed.

She has a new advisor at [name redacted] that has her in a few mutual funds and has 60% of her equity exposure in seven stocks that he changes two to four times a year. I spoke with him and he’s insistent on keeping seven stocks to “juice” her returns.

Should I just cut her losses and move her IRA to an account where she can be in a target date fund or a Bogle three-fund portfolio? Is there anything I’m missing or any reason she should stay with her current advisor? Am I crazy for thinking that 60% of your equity exposure in seven stocks is way too risky for most people?

It’s generally wise investment behavior to ignore short-term performance since long-term returns are the only ones that matter. But at some point you have to benchmark your performance in some way.

I had a neighbor a number of years ago who was always out in his garden. My wife and I would see this guy working away for hours and hours but we could never figure out exactly what he was doing because his landscaping still looked like crap.

Lots of weeds in the mulch. Spotty grass areas. Overgrown flowerbeds.

There’s nothing wrong with being in the garden all of the time if you enjoy being outside but it would have been nice if his time out there actually produced some results.

It sounds to me like your mother-in-law’s financial advisor is a lot like my old neighbor. Sure, they’re doing stuff in the portfolio but not producing much in the way of results for her performance.

If we wanted to take this analogy a step further, I would say he’s been growing a lot of weeds too.

My biggest concern here beyond the performance numbers is the concentration risk they’re putting her through.

There are two types of risk when investing:

Necessary risk is the uncertainty you take when putting your capital to work in the financial markets. You have to invest your money into something if you wish to grow it over time.

Unecessary risk is the risk that’s specific to your chosen investment strategy or behavior.

Holding the majority of your stock market exposure in just 7 stocks is a form of unnecessary risk because it’s so easy to diversify your portfolio these days. The range of outcomes increases exponentially when you hold fewer and fewer stocks.

Sure, a concentrated portfolio gives you the opportunity to outperformance but it drastically increases your chances of underperforming which is likely what’s going on here.

The idea of trying to “juice” your returns to make up for past losses is a recipe for disaster. This is how mistakes can compound in the markets. Doubling down after a period of underperformance doesn’t guarantee you anything but more risk.

Ben’s rule number one for financial advisors is do no harm. This advisor is not following this rule.

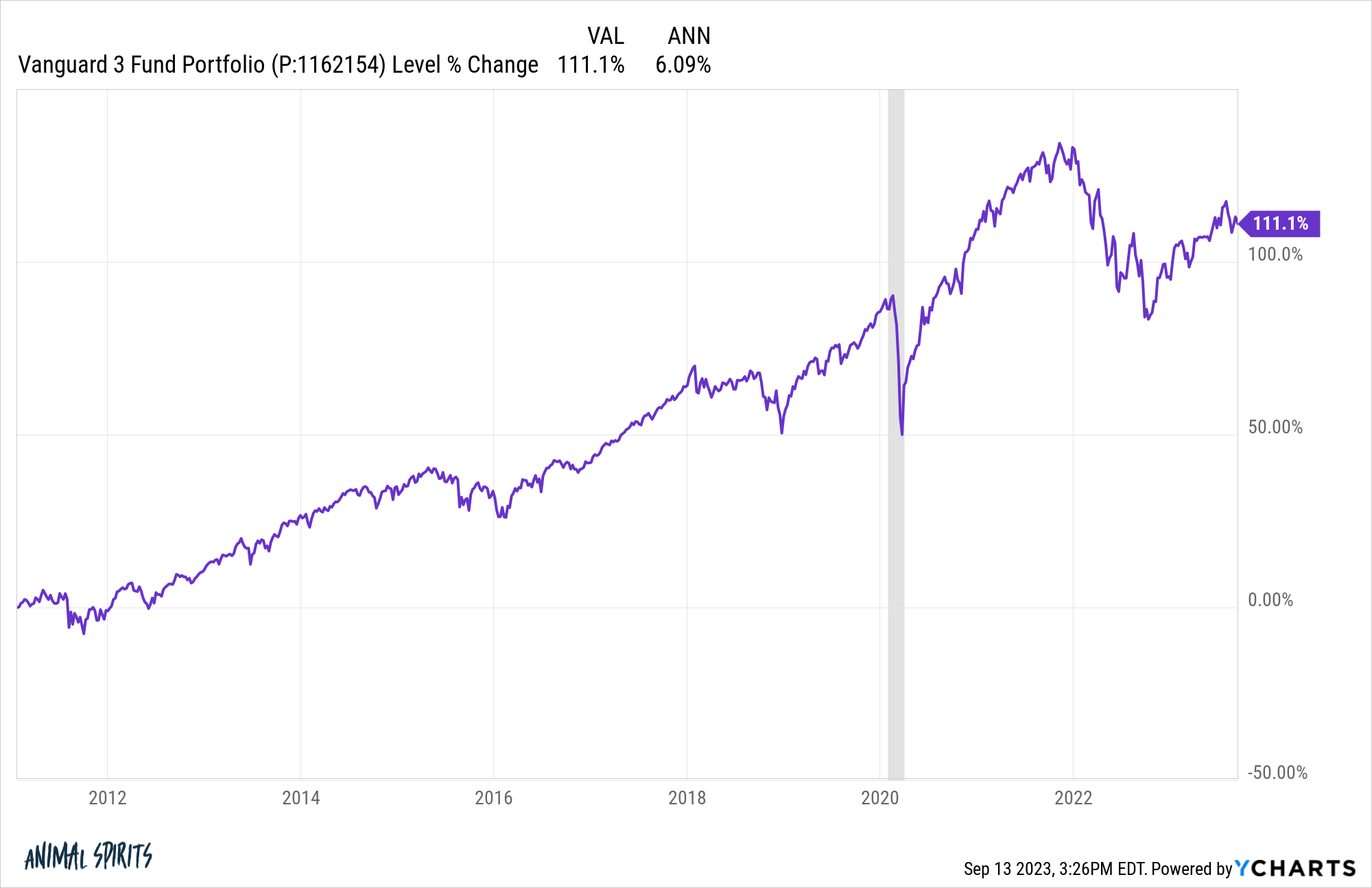

Let’s look at a simple Vanguard three fund portfolio1 to see how badly her portfolio has underperformed. Here are the results since October 2010:

So we’re looking at 6.1% per year versus 2.6% per year.

Let’s say your mother-in-law had a $500k portfolio in October 2010. Her 2.6% annual return would have grown it to around $740k.

Had she been in a simple Vanguard portfolio, it would have grown to more like $1.1 million.

Yikes.

I’m not saying a three fund portfolio is the only answer here. It’s a decent starting point as a benchmark but I would also ask your mother-in-law if she’s getting anything else out of this relationship.

If her advisor is only helping her with investment management, they are not only doing a poor job of it, but there are other ways they could add value.

There is so much more that goes into being an advisor beyond portfolio management — financial planning, tax planning, insurance planning, estate planning, withdrawal strategies, budgeting and helping people make more informed financial decisions.

If they’re simply investing her money and doing so by picking 7 stocks that’s not a financial advisor — it’s a stockbroker (and not a very good one).

So it’s probably not as easy as putting her into a Vanguard portfolio and calling it a day. She needs help understanding what’s going on with her investment plan, right or wrong.

You also have to be careful how you approach this conversation.

This was an expensive mistake. People don’t like talking about financial mistakes, which is one of the reasons there can be so much inertia when it comes to making a change like this.

There’s also a good chance your mother-in-law didn’t even know how bad things were because the advisor has likely been making up excuses along the way.

Don’t make her feel bad about what happened here. Help her learn from her mistakes. Work with her on finding someone who can help right the ship, diversify her portfolio and manage risk in a more prudent manner.

I would suggest you help her find someone who can help her create a comprehensive financial plan, set realistic expectations up front and be more transparent about how they are managing the money.

It’s perfectly reasonable to outsource your portfolio management but you cannot outsource your understanding about what’s going on with your money.

We discussed this question on the latest edition of Ask the Compound:

We also covered questions about buying a vacation home, using CDs instead of bonds, financial struggles with kids and gambling on sports.

Further Reading:

7 Simple Things Most Investors Don’t Do

1Total US stock index fund (35%), total international stock index fund (25%) and total bond index fund (40%).