A reader asks:

If you don’t see it coming, how do you plan for it?

This question was in response to my 10 rules for dealing with uncertainty.

I loved the movie The Holdovers. What can I say? I’m a sucker for a coming-of-age movie.

Paul Giamatti plays a history teacher at a prep school for boys. This line stuck with me when Giamatti describes the importance of studying history to one of his students:

History is not simply the study of the past. It is an explanation of the present.

My read on the past after studying a lot of history is that the future is unpredictable.

One of my favorite examples of this is a memo written by Pentagon staffer Lin Wells to George W. Bush titled Predicting the Future.

Wells described every momentous shift in geopolitics by decade going back to the start of the 20th century. Here’s some of the text:

If you had been a security policy maker in the world’s greatest power in 1900, you would have been a Brit, looking warily at your age-old enemy, France.

By 1910, you would be allied with France and your enemy would be Germany.

By 1920, World War I would have been fought and won, and you’d be engaged in a naval arms race with your erstwhile allies, the U.S. and Japan.

By 1930, naval arms limitations were in effect, the Great Depression was underway, and the defense planning standard said, “no wars for ten years.”

Nine years later World War II had begun.

By 1950, Britain no longer was the world’s greatest power, the Atomic Age had dawned, and a “police action” was underway in Korea.

The memo continued like this until the conclusion:

All of which is to say I’m not sure what 2010 will look like, but I’m sure that it will be very little like we expect, so we should plan accordingly.

This letter was sent in April 2001, just months before the 9/11 terrorist attacks. The 2000s decade included two wars, a massive housing market crash and the biggest financial crisis since the Great Depression.

No one could have possibly predicted those outcomes ahead of time.

As important as it is to study history in order to understand the present, you don’t have to go back that far to understand this idea. The 2020s have already been just as unpredictable as ever.

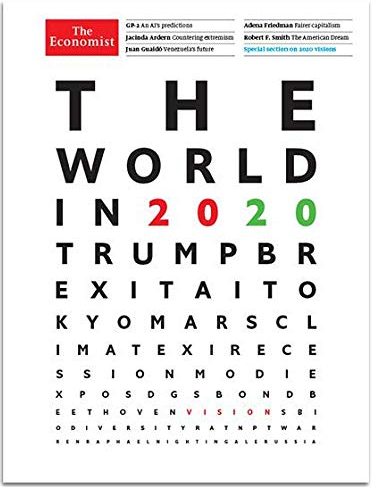

The Economist produced a cover story in November 2019 with forecasts from experts about what might transpire in 2020:

Their prediction list included things like a contentious Presidential election, Brexit, low/negative interest rates, U.S.-China relations, etc.

Guess what wasn’t in there?

A pandemic that would shut the world down, cause governments around the globe to unplug the economy, then plug it back in by sending out trillions of dollars to citizens and businesses alike.

How could you possibly predict that?

Here’s what else no one predicted coming into the 2020s:

- Oil prices turning negative.

- Supply chain shocks.

- The fastest stock market crash and recovery in history.

- The strongest labor market in a generation.

- 9% inflation that wouldn’t lead to a recession.

- AI saving the economy with the release of ChatGPT right as inflation was peaking.

- The Tariff Tantrum following Liberation Day.

I could keep going. None of it was predictable. If you tried to build a portfolio by predicting events like this it would be insane.

So what’s the solution?

How do you plan for this stuff if you can’t predict it in advance?

Some thoughts:

You accept uncertainty as the starting point. Admitting that you don’t know how the future will play out is freeing in some ways. It forces you to focus more of your time on what truly matters.

You set expectations. A good plan does require baseline expectations with the understanding that there are outlier events. But you must recognize the difference between things that could happen and things that usually happen. A good plan takes into account things that are probable, not everything that’s possible.

You build a wide range of results into your plan. I expect to see bull markets, bear markets, expansions, recessions, booms, busts, high rates, low rates, high inflation, low inflation, financial crises and more. But I have no idea when these environments will occur, how long they will last or the magnitude of the moves.

You plan on these things happening but have no control over when or why. And timing these events is impossible.

You create a rules-based plan. Automating good decisions in advance removes the need to predict what comes next.

You focus on what you control. You have no control over the future, what politicians do, geopolitical events, the economic cycle or the timing of bull/bear markets. You do control your risk profile, time horizon, asset allocation, investment expenses and reaction to the events of the day.

You extend your time horizon. Unexpected events can have an impact over the short run but tend to get smoothed out over the long run.

You diversify across scenarios. It’s impossible to diversify away every risk so you try to make your portfolio durable enough to handle different scenarios. That means diversifying across asset classes, geography, market cap and strategy.

You make course corrections along the way. Financial plans are not set in stone. You can update your plans as circumstances change. You need to be flexible in an ever-changing world.

Bill Sweet joined me on the show again this week to answer this question on Ask the Compound:

We also discussed questions about in-plan Roth conversions, how box-spread ETFs work, using a 529 plan for education later in life and how much is too much for private illiquid investments.

Further Reading:

Why History Gets Stuff Wrong All the Time