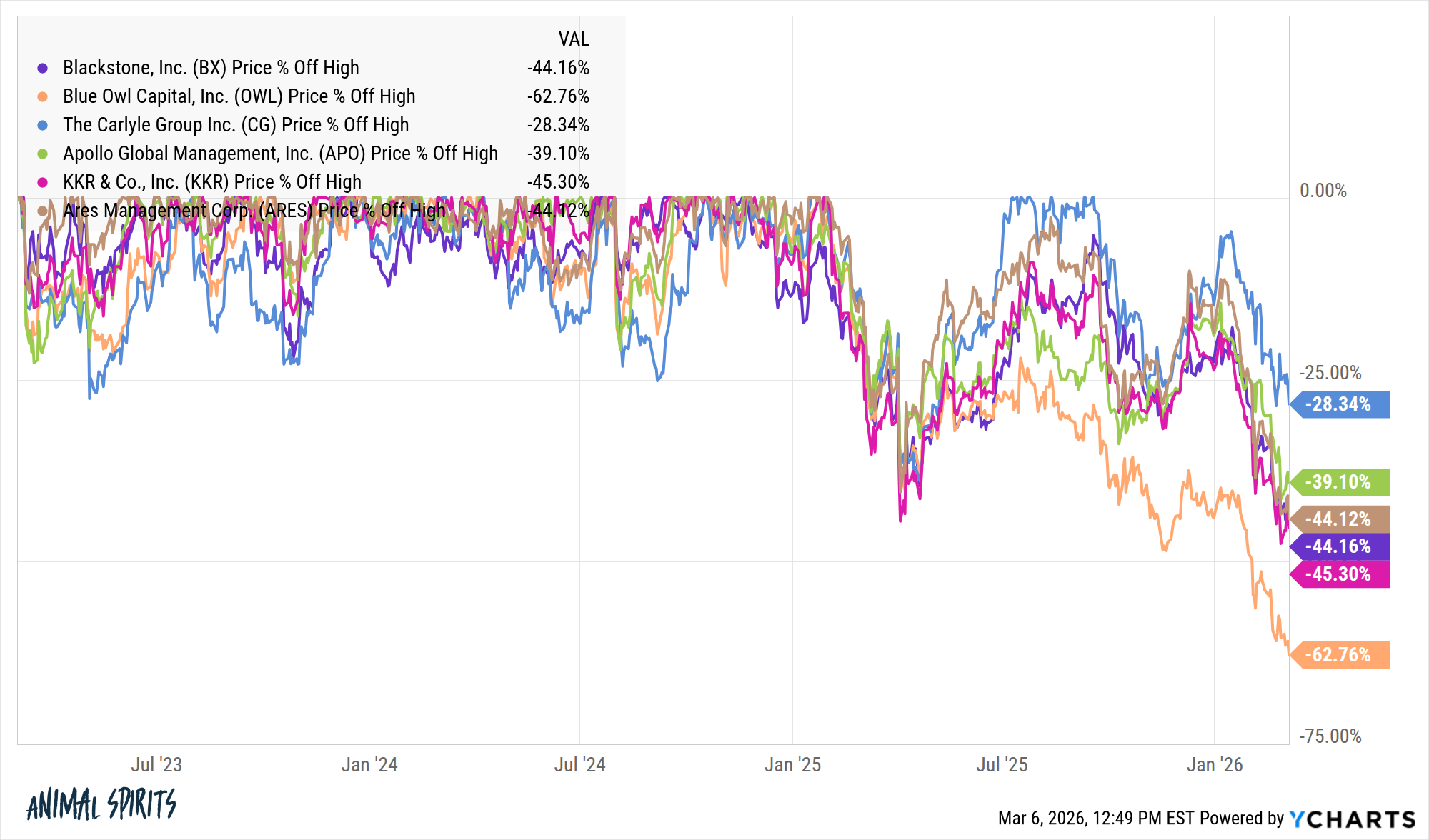

The private equity complex is in the midst of a nice little crash at the moment:

What’s going on here?

Private credit headlines are bad. I called these stocks private equity but the truth is they also manage private real estate, private credit, hedge funds, etc. And the biggest eyesore right now is private credit.

Just look at the recent headlines:

Investors are worried about these funds, they’re trying to pull their money and the sentiment is somewhere in the range of poor to Not great Bob!

Are things really as bad in private credit funds as the headlines would make you believe? We shall see.

Investors don’t care about fundamentals right now, they care about optics.

And the optics are bad.

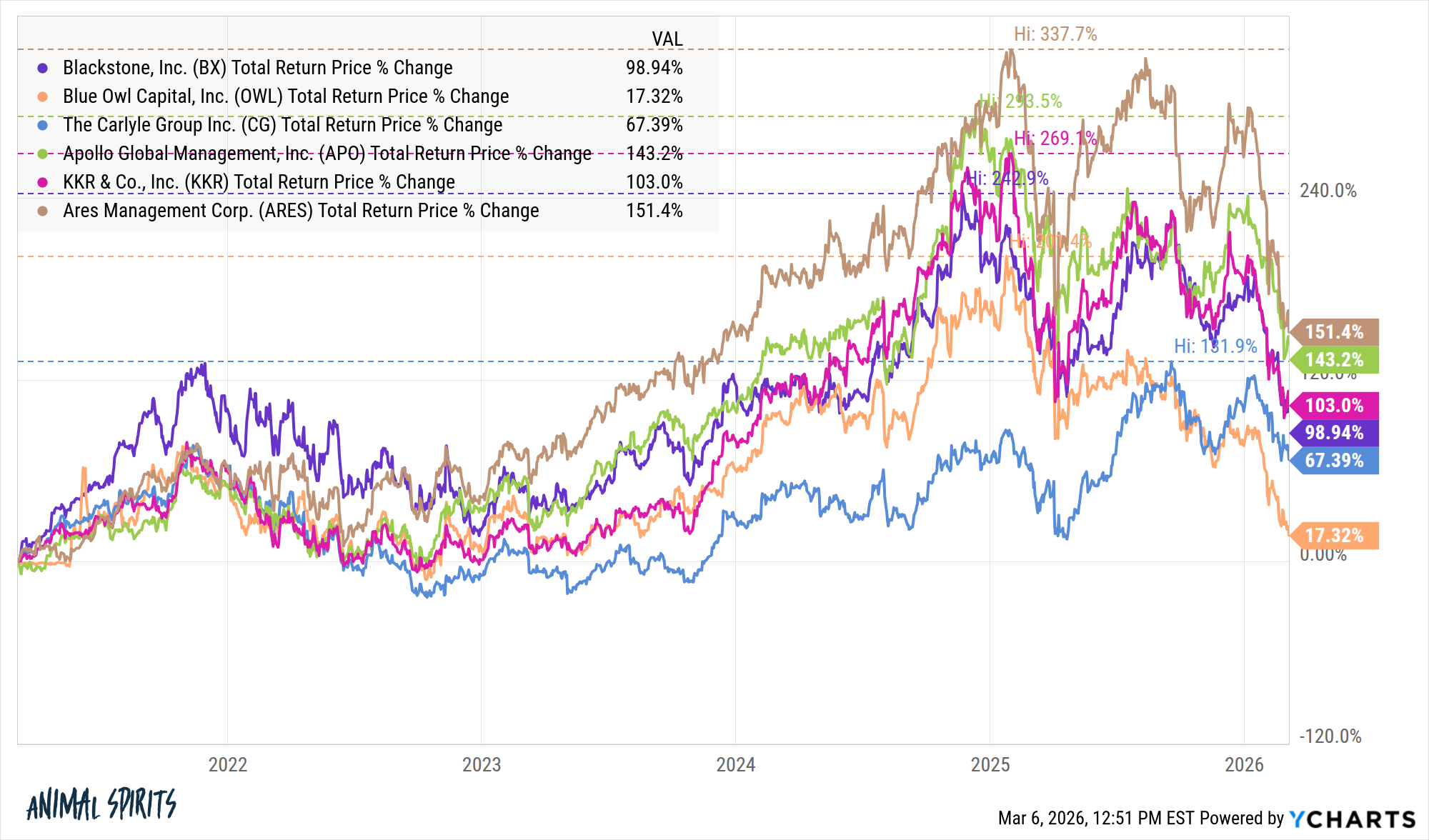

Returns were good. It’s also true that the returns in this space this cycle were really good before they crashed:

Sometimes good returns lead to bad returns.

Software. In times of technological innovation, investors are typically looking to pick the winners. At this point in the AI cycle, investors are more focused on the losers.

Software stocks were getting killed in recent months as investors worried that the moats surrounding these companies were severely tarnished by AI.

Then someone figured out something like 25% of all private credit was invested in software loans. Someone in the private credit space might dispute this number but whatever it is, there is software exposure in private credit and investors don’t like that right now.

The asset-liability-expecations mismatch. Institutional investors have had high allocations to private investments for a while now so the private market managers needed a new source of flows. This explains the big push into the wealth management space in recent years.

The problem is there is that financial advisor clients aren’t like endowments and foundations with a time horizon of forever. Right or wrong, institutions can accept more illiquidity risk.

Individual investors might say they’re comfortable with illiquidity risk but most likely aren’t there yet.

This week on Ask the Compound someone asked:

My financial advisor has me in alternative assets (PE, VC, Private real estate, private credit, etc.). About 40% of my total investable assets (more in brokerage than IRA). I understand the assets – many are semiliquid or illiquid. I’m more interested in what is a reasonable proportion to hold. I am in my mid 40s. Looking to retire in a decade-ish.

Forty percent invested in private markets is a high number regardless of your time horizon. But if you plan on retiring in 10 years or so, that number is dangerously high.

Distributions from PE and VC funds have slowed to a crawl. The IPO market is not picking up steam. These funds can often tie up your money for anywhere from 10-15 years at time. That’s not a bad thing if you have the ability to wait but if you need the money you’re out of luck until you start seeing some liquidity events.

Interval funds typically allow up to 5% liquidity on a quarterly basis but this gets tricky when more and more investors all want out at the same time.

Lots of money has been flowing into private credit in recent years. How does this impact the lending market if they have to pull back? What happens when there is an actual credit event in the economy? Will more and more investors look to get out of these funds now that there is some fear in the space?

I don’t know the answers to these questions. Neither do investors in these companies.

That uncertainty is a big reason why these stocks are selling off.

Is it a buying opportunity?

If the wealth management channel sticks it out or puts a lot more money into this space it might be.

At this point you need to model human behavior more than numbers to guess what happens next.

Michael and I talked about the private equity crash, what’s going on in private credit and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

Organizational Alpha

Now here’s what I’ve been reading lately:

Books:

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures here.