A reader asks:

I have $1.6M in a taxable brokerage account, $250k in a traditional 401k and another $150k in cash. No debt. No house. I’m single with no dependents. I need $170k in annual income to retire. At a 4% withdrawal rate I’d need $4.25M to meet that income goal. In recent years, covered call funds have become popular. For example, SPYI “yields” 12%. That means $1.4M invested would yield $170k per year. Is this too good to be true? Why is this a bad idea? I’m 42 years old and miserable. I own a small business and have worked nearly every day for over a decade. I don’t know if I can do it anymore. I’m totally burned out and want to be done with it.

The investing question here is an interesting thought exercise from a numbers perspective but the small business angle is far more important from a human perspective.

Let’s start with the numbers since that’s the simpler part of the equation.

I’ve written about covered call strategies before. Here’s the explanation I gave a few years ago:

A call option is a contract that gives the buyer the right to purchase a security at a predetermined price at some point on or before a predetermined date. The seller of that call option has an obligation to sell the security at that predetermined price if it happens to make it there by the predetermined date.

If the stock never reaches the strike price in that time frame, the buyer is only out the premium paid while the seller keeps the option premium regardless.

For example, let’s say you own 50 shares of a stock that’s currently trading for $20. Call options with a strike price of $25 cost 50 cents a piece so you would earn $25 in income on your $1,000 position. That’s good enough for a yield of 2.5%.

But now your upside is limited to a 25% gain (going from $20 to $25) plus that 2.5% option premium.

If the stock goes to $30 or $35 you’re out those excess gains over and above $25 and the option buyer is out their $25 in premiums.

In a covered call strategy, you are the seller of call options on your individual holdings or an index.

Thus, this is the type of strategy that should underperform in a rip-roaring bull market. The income from the sale of options can help but in a hard-charging bull market but you’ll likely miss out on some gains and lag the overall market.

However, in a bear market, this strategy should outperform the market because the option income acts as a buffer. Plus, in a bear market, volatility spikes which should actually increase your income since volatility plays a large role in the pricing of options.

Covered call funds became all the rage following the 2022 bear market because of the fact that they outperformed in a down market and come with high yields to boot.

Covered call strategies are perfectly reasonable as a way to reduce equity volatility and increase your income. But you need to understand how these funds work when it comes to the income component.

The yield on a covered call strategy isn’t the Holy Grail many assume it is. You’re not necessarily defeating the 4% rule just because the yield is so high. You need to consider total return, not just the income component.

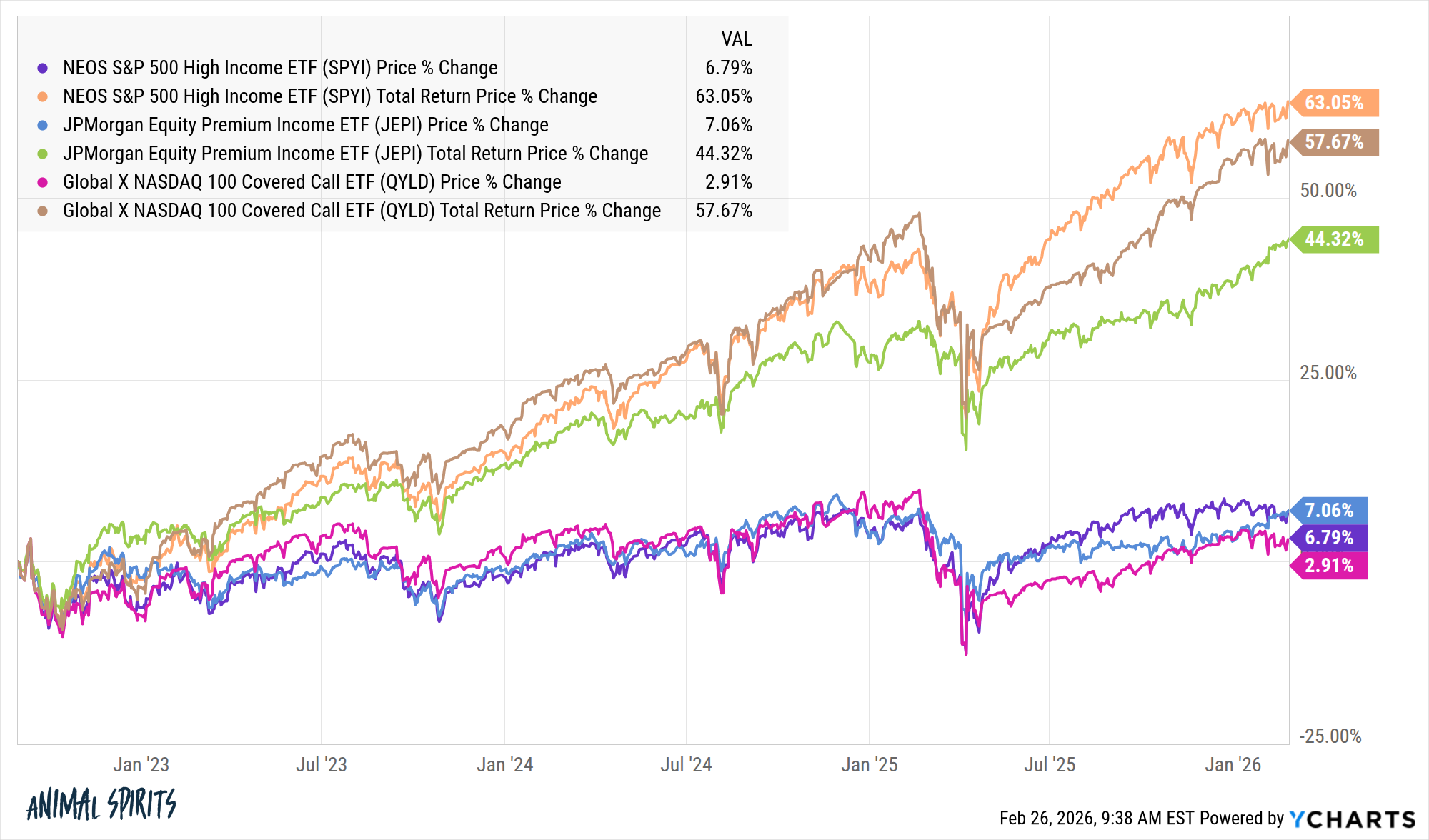

For example, take a look at the difference between the price return and total return on a handful of the biggest covered call strategies:

The total returns are pretty good over the past few years. But look at the price returns. They’re essentially unchanged.

This tells you that basically the entire return has come from the yield. There’s nothing wrong with that per se, unless you plan on living on the income. If you’re spending the yield component of these funds and not reinvesting it then inflation becomes a big risk.

This is especially true if you’re trying to retire in your 40s. A 3% inflation rate would make one dollar today worth 40 cents in 30 years.

Your income also becomes far more variable in these funds. Covered call strategies should fall less than the overall market during a downturn because of the income component but they still own stocks. During the Liberation Day sell-off last year these funds were down anywhere from 16% to 22%.

In a prolonged bear market, your income goes down too.

Covered calls could absolutely play a role in the income portion of your portfolio but there’s more to it than the listed yield.

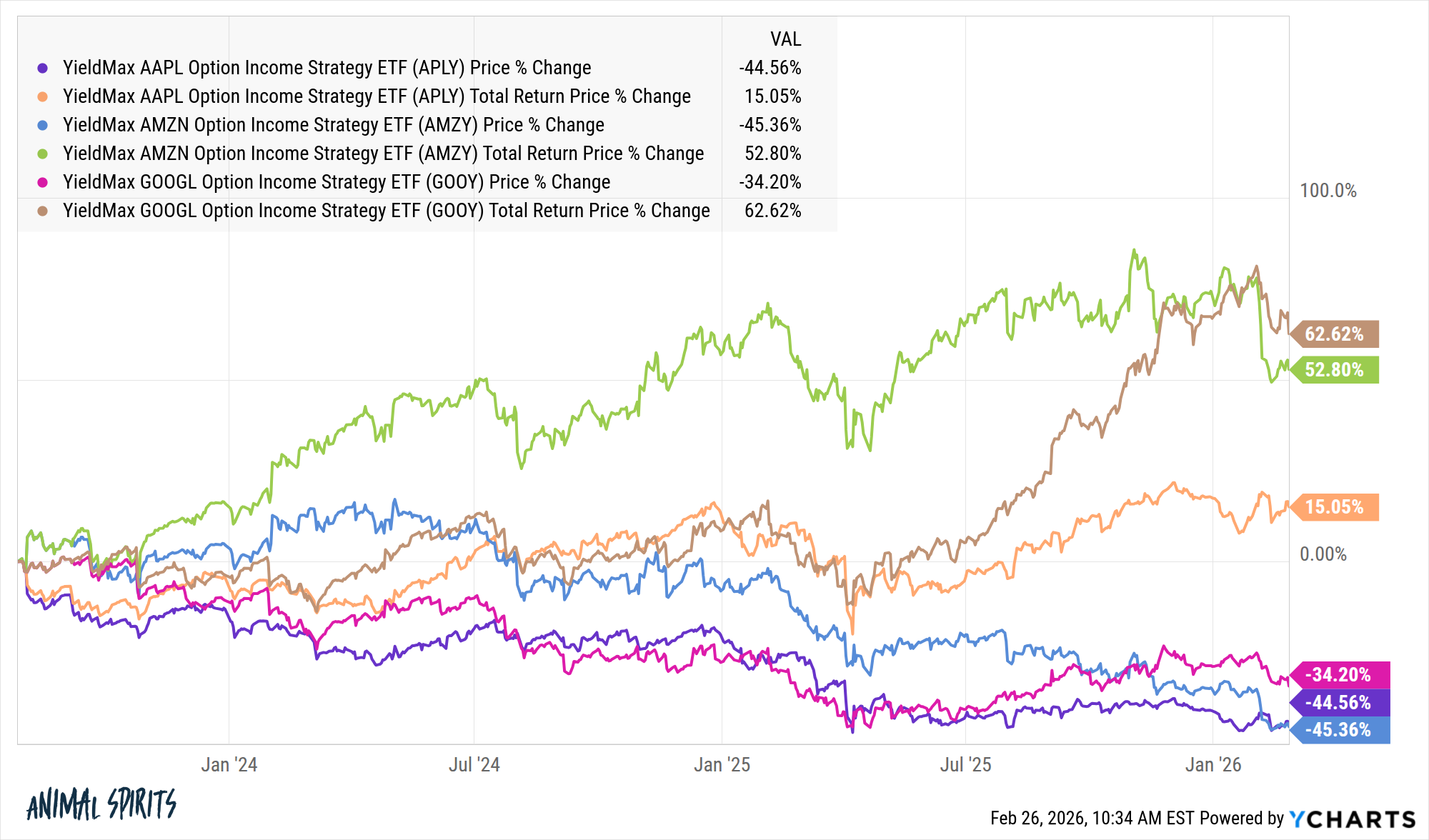

I would be remiss if I didn’t mention the single stock covered call strategies that have become all the rage in recent years. YieldMax has ETFs that sell calls on individual stocks. Right now the covered call ETFs for Amazon, Google and Apple yield 43%, 39% and 37%, respectively.

Sounds great, right?

Look at the difference between price and total returns for these funds:

There is no free lunch. Higher yields mean higher risk. And risk never completely goes away either.

The good news is you’re 42 years old, worth $2 million and have no debt. That’s a huge accomplishment.

The bad news is you’re working too much and it’s making you miserable.

This is a good reminder that running your own business can be highly lucrative but also requires a ton of work.

If you want to spend $170k a year on a $2 million portfolio, that’s a withdrawal rate of 8.5%. There’s no margin of safety at your age because the money has to last you a very long time.

You could turn down the dial on your spending.

You could try to sell the business.

You could hire a manager for the business and extract yourself from the day-to-day.

With no dependents, you have enough money to take a year or two off to figure out what you want to do next.

Maybe you don’t have enough money to live off the dividends at your current spending rate but you have plenty of money to take a break and reassess what you want to do with your life.

Money might not be able to make you happier but it can make you more comfortable and relieve some stress.

That should be your goal.

Bill Sweet helped me tackle this question on an all-new Ask the Compound:

We also answered questions about box spread loans, retirement plans for small businesses, Coast FIRE and tax-efficient asset location strategies.

Further Reading:

Can Covered Call Options Serve as a Bond Replacement?