There’s a personal finance cliche that debt is the devil.

This makes sense to me when it comes to onerous debt like carrying a credit card balance.

But the more time I spend in wealth management the more I realize that the intelligent use of debt can make sense even if you have a high net worth. Lots of rich people use debt as a tool.

When Mark Zuckerberg bought his California home, he took out a 30-year fixed-rate mortgage. Elon Musk reportedly has multiple mortgages on multiple properties.

Why would rich people borrow money?

There are a few reasons.

You don’t want to sell other assets and incur taxes. You don’t want to interrupt compounding. You want to diversify and avoid putting too much cash in one asset. Debt can also be an inflation hedge over the long run.

These reasons aren’t just for mortgages. People also borrow against their portfolios. I know this is sacrilegious to some but it can be a useful form of debt under the right circumstances.

Obviously, the biggest risk when borrowing against your portfolio is getting a margin call. You need to think long and hard about the amount of money you borrow and understand how a stock market crash could impact this type of loan.

Having said that, portfolio loans are extremely flexible. Getting a loan through the bank can be an annoying process with loads of paperwork and headaches. Portfolio loans can go through much faster.

Most major brokerage platforms and banks offer securities-backed lines of credit (SBLOCs) that allow you to borrow against your portfolio.

One of the downsides of these loans is that the borrowing rates can be relatively high, something like the risk-free rate plus 2-4% or so. That ends up being higher than mortgage rates for most borrowers.

However, there are other options now.

Bloomberg had a story late last year that got a lot of attention from financial advisors and wealthy investors alike:

Here’s the lede:

In late 2021, as the housing market overheated and the Federal Reserve’s benchmark interest rate hovered near zero, Tony Yang found an unconventional way to fund his down payment.

He logged into his Charles Schwab brokerage account, built a trade he’d discovered on Reddit — and unlocked about $650,000 to help finance a Bay Area home.

The trade, dubbed a “box spread,” carried a kind of mystique. By combining two opposing options positions — one bullish, one bearish — Yang built a strategy that mimics a fixed-rate loan: upfront cash now, repayment at a set date, and a locked-in cost in between.

Yang used it to borrow at just 1.6% for five years — well below the rate on his traditional mortgage — creating a down payment without having to sell assets he wanted to keep in the market.

That 1.6% box spread financing rate was back when interest rates were much lower. It’s higher now because rates are higher.

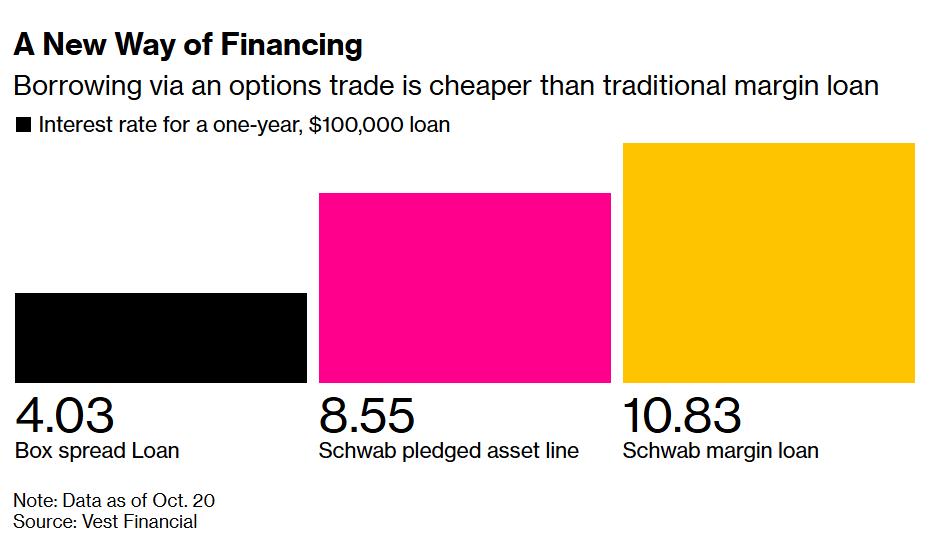

But look at Bloomberg’s comparison of more recent borrowing costs:

Using your portfolio as collateral for a box spread loan offers a much lower interest rate, closer to the risk-free rate.1

I am not an options trader but allow me to explain how these box spread loans work from the perspective of the borrower at a high level:

- You use your portfolio as collateral for an options position.

- How much you can borrow depends on the securities.

- The length of time varies from month to month up to around five or six years.

- There are no monthly payments.

- There is no interest due until the expiration date.

- The “interest” paid on the loan is actually considered a loss for tax purposes.

- At expiration of the loan you can choose to pay it off or roll it over into a new box spread position.

If you have no experience with these instruments, this topic can range from sounding too good to be true to an overwhelming feeling where it’s difficult to understand.

So I had Joseph Wang from SyntheticFi on Talking Wealth to dicuss:

- How box spread loans work.

- Why these loans are relatively new for some but have been around for a long time.

- The use cases for these loans.

- My personal box spread scenario.

- How SyntheticFi works with financial advisors.

- The risks involved in the process and more.

Watch here:

Podcast version here:

Subscribe to our Talking Wealth newsletter here.

Further Reading:

Why I Might Never Pay Off My Mortgage?

1Depending on the duration of the loan that turns out to be similar to Treasury rates at similar maturity levels, plus whatever the fees are.

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures here.