A reader asks:

The “Relentless Bid” of 401ks has inflated stock prices and dampened volatility for years. As the population ages, target-date funds are swapping stocks for bonds, and people have to take RMDs. At what point does this cavalcade of selling drive stock prices down, and become the “Relentless Beg” (or “Relentless Ask” if you prefer)? Or is wealth so top-heavy that this phenomenon is just too small to make a difference?

I’ve been getting some variation of this question for the past 10 years or so.

It makes sense in theory.

Josh wrote about the Relentless Bid back in 2014. Here’s the main takeaway:

What this means for the very character of the stock market and the way it behaves is very important. It means that, almost no matter what happens, each week advisors of every stripe have money to put to work and they’re increasingly agnostic about the news of the day. They’ve all got the same actuarial tables in front of them and they’re well aware that their clients are living longer than ever – hence, a gently increased proportion of their managed accounts are being allocated toward equities. And so they invariably buy and then buy more.

A combination of tax-deferred retirement plans, improved technology, lower costs, and new default rules has led to an automatic investing revolution. It’s a glorious step forward for investors and baby boomers were at the forefront of this trend.

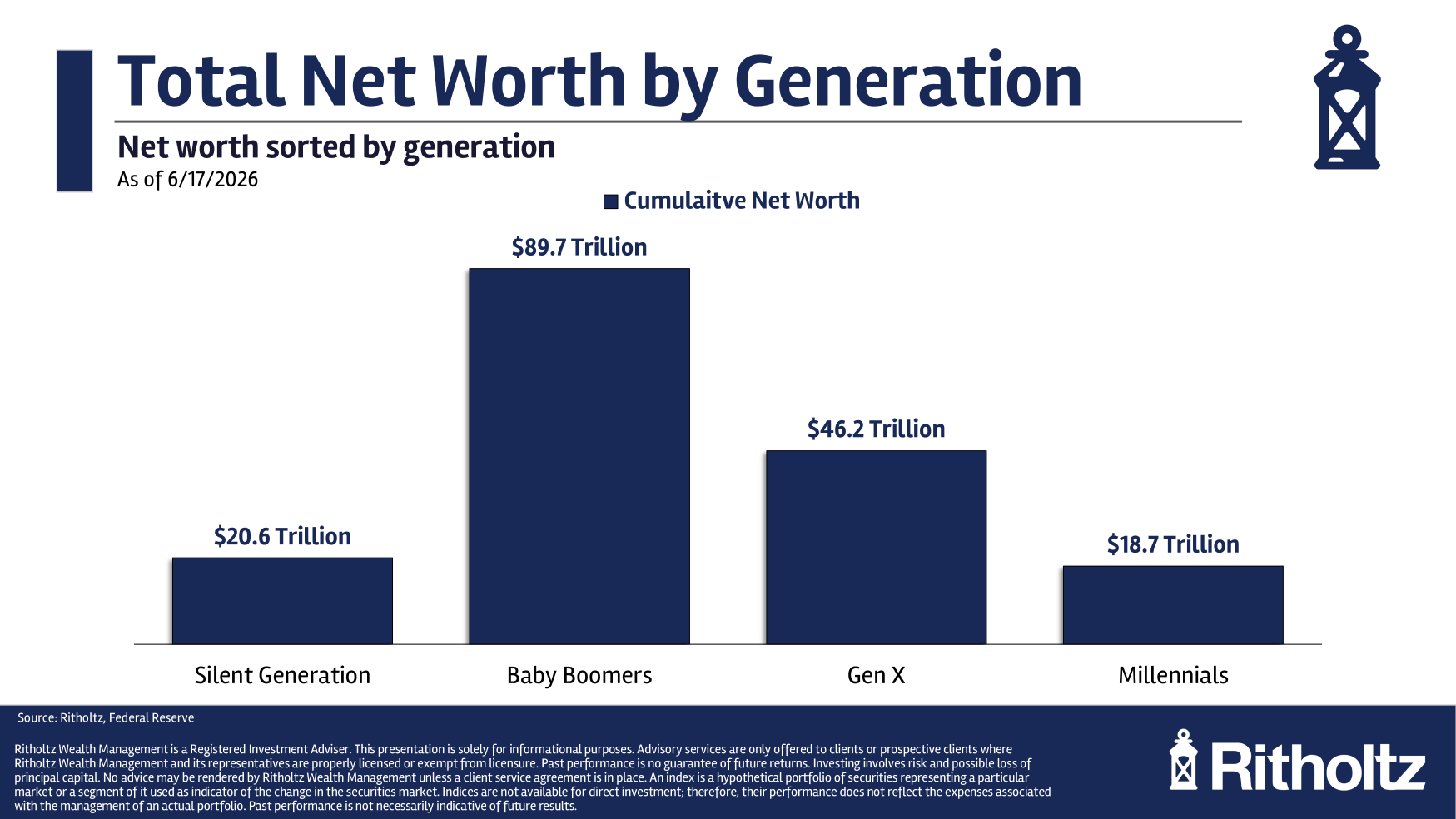

And they are by far the richest generation in history because they’ve been buyers of financial assets for many decades:

Baby boomers are worth around $90 trillion in total net worth but it’s probably higher than that. The Silent Generation still controls $20 trillion in assets and that’s people who are 81 and older. Most of that money is getting passed down to the boomers so they actually have more like $100 trillion.

The baby boomers and older own nearly 70% of the stocks. They also control half of all the housing market wealth too.

They’ve been the biggest buyers of stocks for years now. What happens when they turn into sellers during retirement?

Somewhere in the range of 40 to 50 million baby boomers are already retired today. Why hasn’t the stock market crashed yet? Surely, there has been some selling from RMDs and retirement needs?

I think the fears of baby boomers crashing the market are overblown for a few reasons.

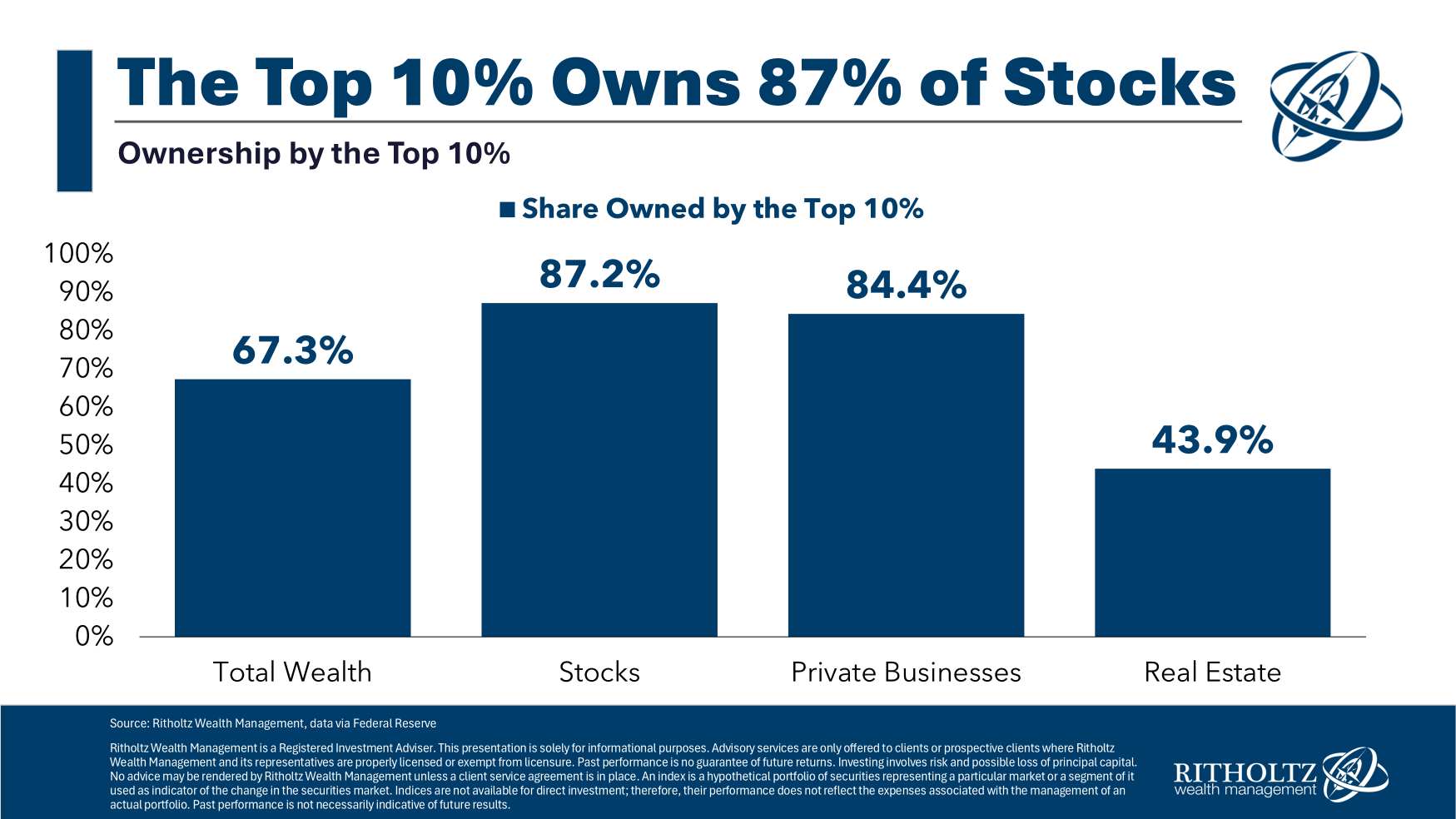

1. Stock market wealth is concentrated. The top 10% controls 87% of the stocks, nearly 85% of private business and almost 70% of total wealth.

Most of this wealth isn’t going to be spent — it’s going to be passed down to the next generation.

Yes there will be some selling of stocks in the years ahead to fund retirement lifestyles but probably less than you think from the entire pie. And those RMDs that are being spent is money that’s being recycled into the economy.

That’s not necessarily a bad thing for corporations if baby boomers keep consuming.

It’s also true that this money will be spent in more of a glidepath than all at once.

2. Baby boomers still need to take risk in retirement. For a 65 year old couple, there is a 64% chance at least one of them will live into their 90s.

If you retire in your 60s, you could have 20-30 years to continue investing and keep up your standard. Retirees still need to take some risk to hedge the inflationary beast.

Stocks will still play a role in more retirement plans because most baby boomers will need to grow their portfolios.

3. Millennials are the offset to the boomers. There are currently 70 million or so baby boomers. That number is expected to decline by roughly 16 million from now until 2035 and another 24 million by 2045.

But there are also 73 million millennials who will be reaching their prime earnings years right as the boomer generation begins to spend down portfolios and die off.

There are a lot of rich old people but more young people who can step up as buyers of their assets:

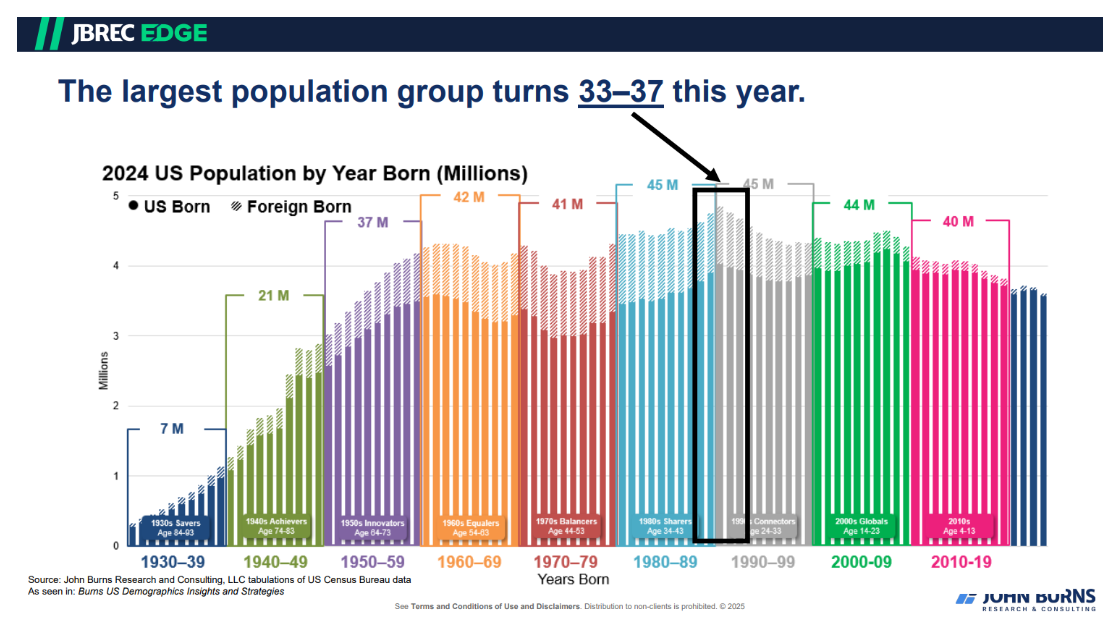

The largest population group this year is 33 to 37 years old.

Young people are investing in far greater numbers than baby boomers did at their age. If there are more stocks or houses available there are willing buyers out there.

The other thing to remember about demographics is that this stuff is relatively straight forward from a planning perspective. This baby boomer demographic cliff is no surprise to market participants. The market already knows this is coming.

We had a lengthy discussion about this question on an all new episode of Ask the Compound:

Bill Sweet joined in to answer questions about time management, student loan forgiveness programs, property taxes, starting your own business and Ray Dalio’s dire market predictions.

Further Reading:

Rich Old People