Households have dealt with a lot of hurdles in the 2020s, economically-speaking.

First there was the pandemic which screwed up supply chains and led to an unthinkable amount of government spending to keep people and businesses afloat.

That led to the highest inflation levels in four decades.

Then the Russia-Ukraine war sent gas prices through the roof.

We also had tariffs to deal with last year.

The Iran war this year sent gas prices shooting higher yet again.

All told prices are now roughly 30% higher than they were coming into this decade. That’s already higher than the price increase for the entire 2010s decade of around 19%.

And yet…people continue spending money:

There hasn’t been a recession since the minor Covid blip despite many forecasts to the contrary.

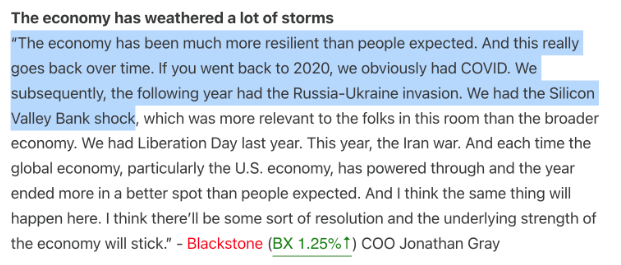

CEOs keep reporting how strong the consumer remains (via The Transcript):

Obviously, it helps that financial assets have risen substantially this decade. The wealth effect has certainly been a driver here.

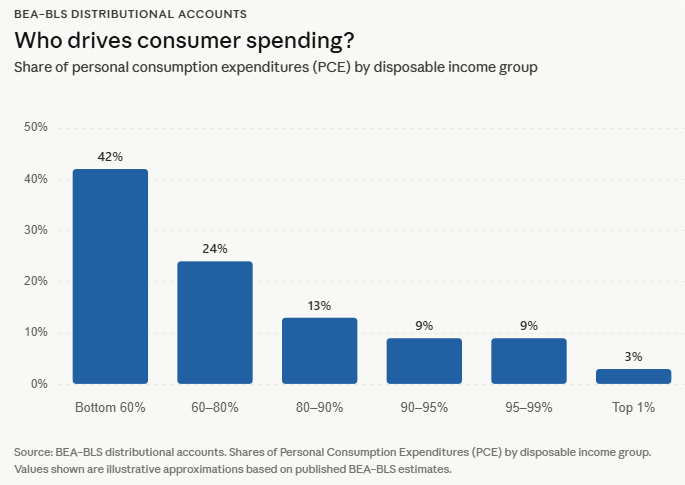

There has been a lot of talk about a K-shaped economy but data from the BEA shows spending is not as uneven as the media would have you believe:

The real K-shaped part of the economy just might be the housing market.

The home ownership rate in this country in 2020 was 65% (roughly where it is today). At that point housing prices were much more affordable and 30 year mortgage rates were around 3%.

If you bought or owned a home before 2022 and took advantage of ridiculously low mortgage rates, you locked in the inflation hedge of the century.

A lot of people did just that.

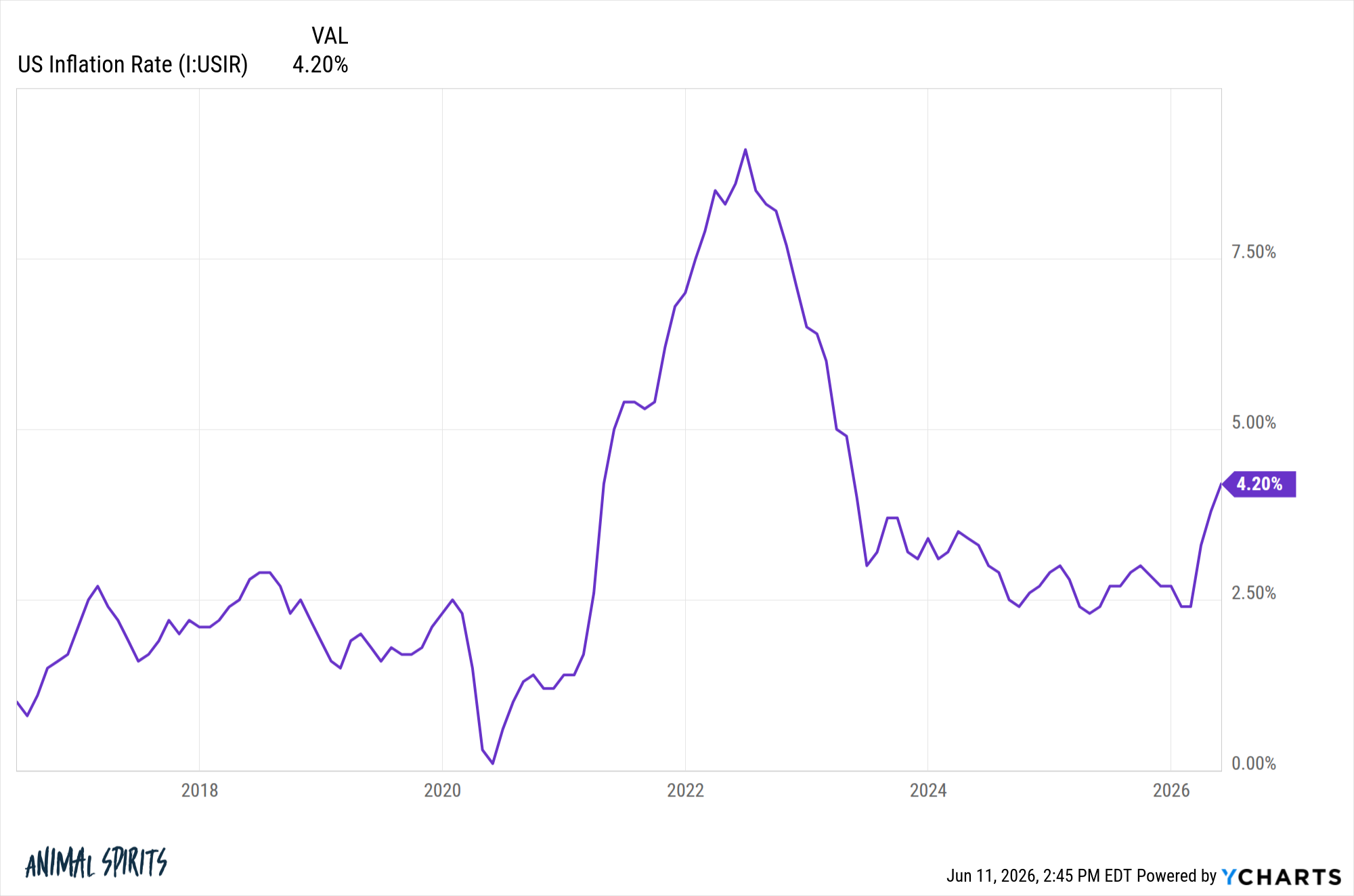

Just look at the inflation rate now:

It’s back above 4% due to a resilient economy and the war in Iran. If you still have that 3% mortgage you are effectively borrowing for free right now on an inflation-adjusted basis.

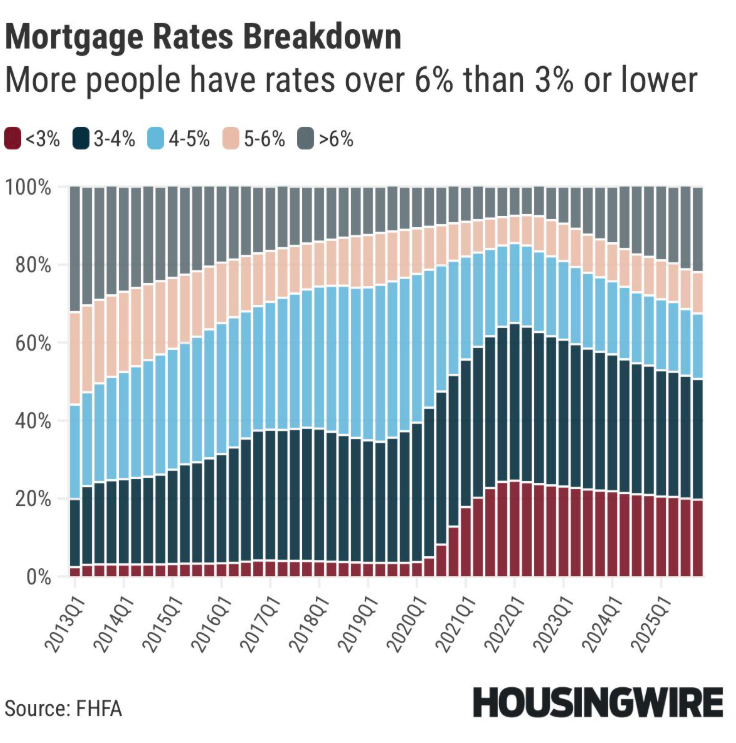

There has been some housing activity in recent years but it’s still roughly half of all borrowers with mortgage rates of 4% or lower:

When you combine this data with the fact that 40% of homeowners own their home free and clear it’s no wonder households have been able to keep spending.

How many people would be able to afford their own home right now at current prices and mortgage rates?

The fact that so many people locked in low mortgage payments have been paying dividends for the economy all decade long.

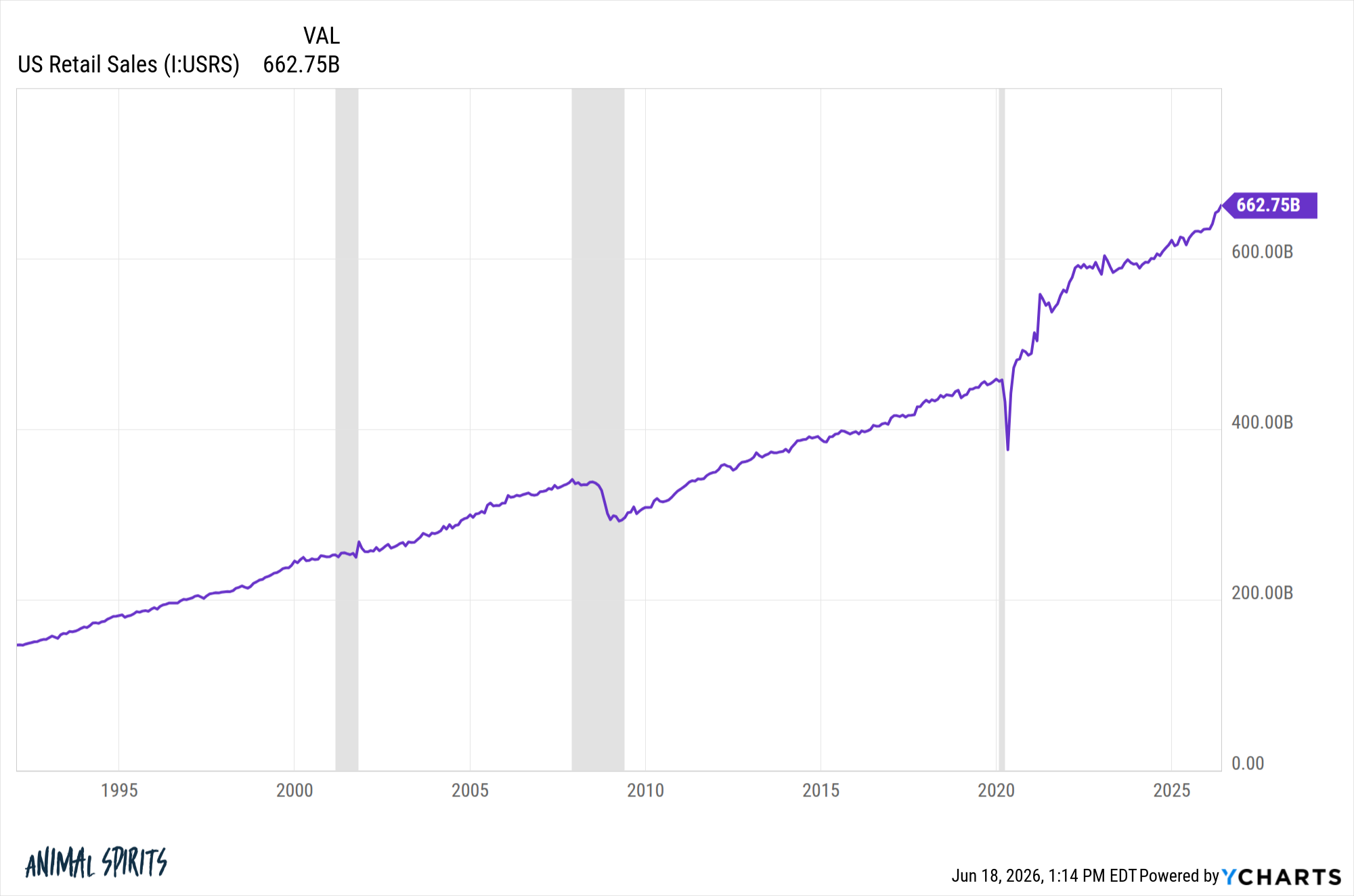

Money not spent on housing can be spent elsewhere in the economy. That’s why retail sales numbers have been so strong. It’s also one of the reasons flows continue to go into the stock market.

Most economic forecasts have been wrong this decade in part because so many people were able to hedge their biggest budget item.

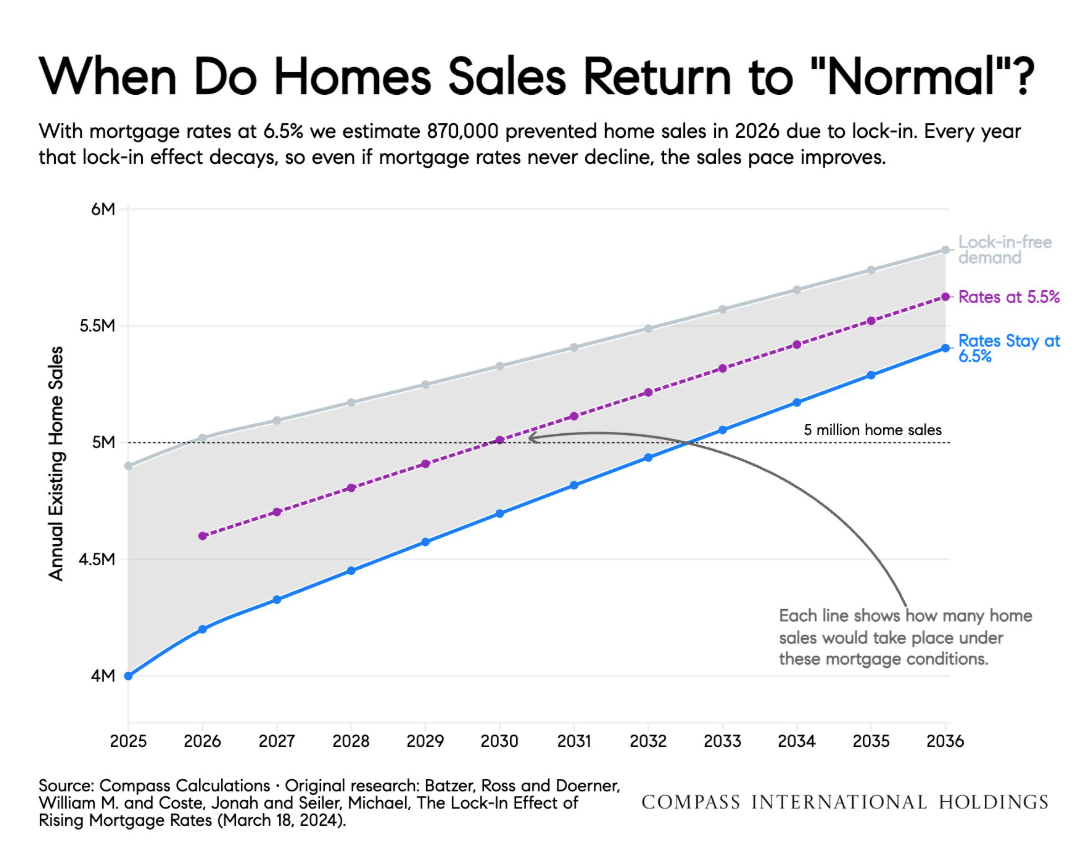

The big question is when does this hedge begin to fade?

Mike Simonsen took a stab at it from the perspective of housing activity:

It could be a while.

Of course, crazy things have been happening to housing throughout the 21st century.

The 2000s started out with a housing bubble.

When it burst we had one of the biggest housing crashes in history.

Prices were extremely affordable throughout the 2010s.

The pandemic pulled forward an enormous amount of demand and price growth.

So maybe there will be an external shock that changes the trajectory of housing prices yet again.

The hard part about the housing market for so many people is that it’s been so predicated on timing and luck.

Many households lucked into lower prices and mortgage rates which combined for the hedge of a lifetime.

Others haven’t been so lucky and now must contend with lower supply, higher borrowing rates and much higher prices.

Michael and I talked about mortgage rates, inflation, consumer spending and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

How Are Consumers Still Spending So Much?

Now here’s what I’ve been reading lately:

Books:

Podcast book tour:

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures here.