My first job in the industry was working as an analyst for an institutional investment consulting firm that specialized in managing money and investment plans for hospitals.

Hospitals might be non-profit but they certainly make a lot of money.

My boss taught me a lot about setting investment guidelines, the importance of asset allocation, risk profile and time horizon. When I first started at the firm, he used a new client to teach me the importance of matching assets with liabilities when constructing a portfolio.

These hospitals all had numerous investment funds to manage — endowments, foundations, pension plans, operating funds, etc. Each one required its own separate allocation and investment guidelines because they had different goals and time horizons.

They also had malpractice insurance funds set aside for lawsuits against the doctors and other medical practitioners when there was a mistake. The new hospital came to us with their entire malpractice fund sitting in cash. The money needed to be paid out so they didn’t want to take any risk.

But my boss knew these claims typically took longer than expected. From the time a claim was made it could be 6-18 months for a simple case to be paid out. More complex cases that went to trial could be anywhere from 3-5 years until a payout was made.

We had them look at the history of malpractice claims and they discovered the average case took roughly three years from the time a claim was filed until a payout was expected.

Sitting on cash led to a mismatch in the asset-liability mix of the fund. They had the ability to take more duration and thus increase the yield on this portfolio. So that’s what we did for them. It wasn’t a huge difference but it was enough of a boost to make the hospital board happy.

This idea of matching your investments with your goals, risk profile and time horizon was drilled into my skull from the early days of my career.

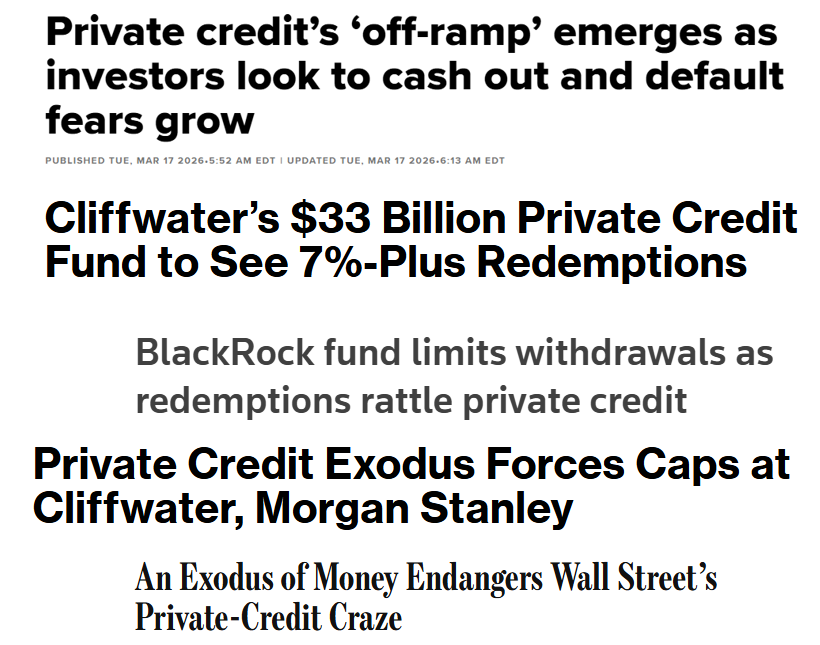

I’ve been thinking about this idea of asset-liability matching regarding all of the headlines in recent months about private credit:

Private credit is essentially the funding market for borrowers who have outgrown their local bank but aren’t quite ready to fund operations via Wall Street just yet. They’re private, direct loans with higher rates because you don’t have to deal with bondholders or overly regulated financial institutions.

Regulations coming out of the 2008 financial crisis made it much harder for banks to make these loans so private market managers like Blackstone, Apollo, KKR, Ares and Blue Owl stepped in.

Like other corporate bonds, you have credit risk if a borrower defaults on the loan. However, the biggest difference between public and private credit is the liquidity, or lack thereof with these loans.

Because the loans are floating rate, meaning they adjust to market yield movements, private credit funds performed much better than most fixed income during the bond bear market of 2022. That, combined with much higher yields, meant billions and billions of dollars flowed into this space in recent years, most of it from the wealth management channel.

The problem is that a lot of the hot money either (a) didn’t set the right expectations with their investors up front or (b) didn’t have the correct time horizon in mind when allocating to the space.

These private loans aren’t meant to be traded. You clip your coupon and hold the loans to maturity. That means you should have a time horizon of at least 5 years, but 7-10 years probably makes more sense.

Interval funds do allow 5% redemptions each quarter but these private loans aren’t meant to be traded in and out of.

This is not a short-term asset class that you should be trying to time by jumping in when rates look juicy and getting out when you’re worried about credit issues flaring up.

I don’t know enough to comment about the credit quality of the private credit space as a whole to make a judgment call on this asset class. A lot of investors and reporters think the software exposure and poor lending standards will lead to some blow-ups. The private credit people say everything under the surface is still fine.

Regardless of how this all plays out, there was an obvious mismatch between this fund structure and the expectations set by the advisors to their clients.

You need to think long and hard about your time horizon for any investment but especially illiquid assets.

There are obviously far too many investors who didn’t think about this before allocating to private credit.

Further Reading:

Why is Private Equity Crashing?